WANAN YOSSINGKUM/iStock via Getty Images

In today’s environment of rising rates and inflationary environment, I wanted to find a high quality stock that is a relatively safer investment in these trying times. MSCI (NYSE:MSCI) came across as an investment idea that could outperform in today’s market conditions. Along with fears of a recession occurring, I think that there is added value in MSCI’s highly recurring revenue model and enviable industry position that could help tide it through difficult times.

Investment thesis

MSCI seems to be an attractive investment in the current market conditions and these are the investment cases for MSCI:

- MSCI has a high quality business model that is majority revenues that are highly recurring, with high retention ratios. This, in turn, brings about strong revenue visibility, highly sticky revenues and lower risks for the business.

- MSCI has several favourable and secular tailwinds for it to sustain double-digit organic revenue growth. This includes the shift from active to passive investing, increasing demand for passive investments outside the US and particularly in Asia, increasing trend of ESG integration and higher demand for alternative investments.

- MSCI is a pioneer and market leader in the ESG and Climate segment, as it continues to provide ESG and Climate data, information and research to the largest asset managers in the world. In addition, its ESG and Climate indices are leading the market with the largest number of equity ETFs and assets under management linked to its ESG and Climate indices.

- MSCI has an industry leading EBITDA margin and attractive free cash flow generation profile, demonstrating its dominance over industry peers as well as its superior competitive moat.

Overview

MSCI is a company that provides tools for making investment decisions. In essence, its offerings help clients to optimise the portfolio construction process. One of MSCI’s key value propositions is its ability to provide end-to-end solutions across multiple asset classes. These solutions comprise of:

- Index tools for indexed product creation, performance benchmarking and portfolio construction

- Analytics for risk management, performance attribution and portfolio construction

- ESG and climate data, ratings and research

- Real estate data and analysis.

When looking at where revenues come from, a large majority of revenues comes from its Index segment (61% of revenues), while its second largest segment is its Analytics segment (27% of revenues). The two smaller segments are ESG & Climate (8% of revenues) and Private Assets (4% of revenues).

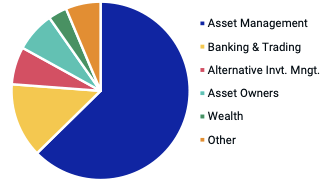

Apart from its end-to-end providing an edge, I think that another advantage it has is the wide range of investment professionals it services, which creates this nice symbiotic ecosystem of solutions and scale combined. MSCI counts asset owners, asset managers, financial intermediaries, hedge funds, wealth managers, insurers and corporates as its clients. In addition, MSCI serves clients in the US and in overseas markets as well.

MSCI Client Segment Mix (MSCI 1Q22 Presentation)

High quality business model

One of the first things I think is attractive about MSCI as a high quality investment is derived from its business model. I think that with the company’s solutions being of value add and essential to its clients in the financial industry, this allows MSCI to run a rather healthy business model based on highly recurring revenues and solid retention rates.

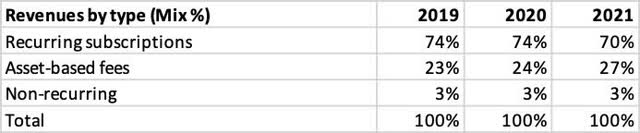

When looking into MSCI’s revenue mix, we can see that 97% of its revenues were recurring in nature. This includes its recurring subscriptions revenues which comprise 70% of revenues as well as its asset based fees, which makes up 27% of revenues. While asset-based fees are recurring in nature, they tend to be more volatile, which I will highlight below in the “Risks” section. That said, with only 3% of revenues that are non-recurring, I like MSCI’s highly recurring business model that would serve as a decent buffer in a tough environment like today.

MSCI revenues by type (MSCI Annual Reports)

On top of that, MSCI has disclosed that its retention rates are more than 90% across all product segments, which in my view shows very strong demand for MSCI’s offerings, as well as the value add that MSCI brings to its customers.

With MSCI’s revenue model being largely recurring in nature and with high retention rates, this brings about the advantage of increased revenue visibility, higher stickiness of revenue streams, and lower perceived risk in the business.

Secular tailwinds in Index, ESG & Climate and Private Assets

On top of a high quality business model, it is also encouraging to see the secular tailwinds that favours MSCI’s segments. I am of the opinion that we could see MSCI sustaining double-digit revenue growth by continuing to cross-sell and up-sell existing customers, bring in new customer wins and new product offerings, as well as to leverage on pricing.

In particular, I think we will continue to see MSCI’s Index segment do well. Recall that this segment represents more than 60% of revenues. This segment benefits from multiple tailwinds, including the continued transition from active investing more towards passive investing. According to Bloomberg, passive investing will likely take over active investing by 2026, and this could happen earlier if a bear market occurs. In addition, MSCI could benefit from increasing global AUM in the near future as there is increasing evidence that more in overseas markets like Asia are also shifting from active to passive investing. Other trends that benefit the Index segment include the increasing use of factors in mainstream investing, as well as the increasing demand for sustainable passive investments. These 2 trends will likely serve as additional tailwinds for the Index segment as MSCI rolls out more products in these areas to capitalise on these trends.

For the ESG & Climate segment, it is benefiting from the increased demand for ESG integration, while the Private Assets segment is benefiting from the increased interest in alternative investments.

Pioneer and market leader in ESG & Climate

I think that we will likely see ESG & Climate be a huge contributor to MSCI’s future growth, and as such this segment warrants further analysis.

MSCI claims to be the pioneer and market leader in ESG & Climate, and this is backed up by the numbers and customers that the segment has been successful in acquiring.

On ESG, MSCI managed to attract 49 of the top 50 asset managers to leverage on MSCI ESG research and as of 1Q22, it has 2,600 ESG clients. I think that the strong demand for its ESG research goes to show the incremental value add MSCI’s ESG offerings bring to the top asset managers. In addition, MSCI is the number 1 ESG index provider by equity ETFs linked to its ESG indices, with almost $579 billion in assets under management linked to its ESG indices.

On the Climate front, MSCI provides climate data to 44 of the top 50 asset managers, and is also the number 1 climate index provider by equity ETFs linked to MSCI’s climate indices.

Industry leading margins

As can be seen below, MSCI has managed to grow EBITDA margins from 52% in 2017 to 59% in 2021, thereby sustaining its industry leading EBITDA margin profile. I am of the opinion that MSCI will still be able to sustain these margins, in the range of mid to high 50% range, which is still higher than the average of 35% margins its peers are seeing.

This industry leading EBITDA margin profile is driven from MSCI’s strong competitive moat, differentiated offerings and operating leverage.

MSCI financials and margins (Author generated)

Also, FCF generation has been solid as it grew by 27% over the 5-year period, and FCF margins have also improved from 28% in 2017 to 42% in 2021. As a result, this demonstrates MSCI’s strong cash generation profile due to its asset-light business model which generates large amounts of free cash flows.

Valuation

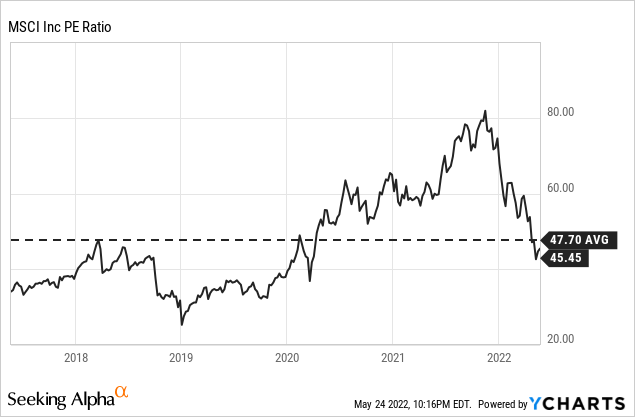

Just by looking at MSCI’s historical P/E ratios, we can see that it has come off from being relatively overvalued at the end of 2021 with a P/E of more than 80x to the current 45x P/E. This is 5% lower than the 5-year average P/E of MSCI and I would argue that this presents an opportunity to add MSCI at a relatively inexpensive valuation.

I derive my target price of $567 by applying a 42x multiple to my 2023F EPS forecast of 13.50. This higher multiple is warranted given MSCI’s industry leading margin profile and competitive moat. This implies a 37% upside from current price levels.

Risks

Asset-based fees

Asset-based fees may be recurring in nature, but they can be volatile as market conditions change. This is because asset-based fees are determined by AUM and trading volume of ETFs linked to MSCI’s indices. As the market conditions year to date has been brutal, this has resulted in lower AUM of ETFs linked to MSCI’s indices due to price depreciation.

When looking into its 1Q22 results for an indication of the impact, there was a price depreciation of $90 billion in 1Q22 from the AUM in ETFs linked to MSCI indices. This was offset by positive inflows to linked ETFs of $20 billion. This means that the total period-end ETF AUM as of 1Q22 was $1,389 billion. Combining the net effects of lower AUM and net inflows, this led to a 4% decrease in total period-end ETF AUM.

As such, for MSCI’s 1Q22 results, the miss in AUM-based fees was -2% vs. consensus, and this was offset by a beat by ESG and Climate of +4%.

Customer concentration

BlackRock (BLK) makes up 13% of MSCI’s revenues. This level of concentration on one customer brings about customer concentration risk. However, there are currently no indications that this working relationship is turning bad. Moreover, the fact that BlackRock, which has more than $9 trillion in assets under management and the largest asset manager by AUM, is such a big customer of MSCI seems to bode well for MSCI and its competitive advantages.

Conclusion

The future looks bright for MSCI. With multiple favourable industry tailwinds supporting the shift from active to passive investing, new styles and factors to invest in as well as the increasing demand for ESG investments, MSCI is positioned well in an industry destined to grow. Furthermore, the fundamentals of the business remain solid. It has a solid and high quality revenue model with highly recurring revenues with solid retention rates, and industry leading EBITDA margins and attractive FCF generation. Lastly, to leverage on the trend of ESG and climate investments, MSCI is well positioned as a pioneer and market leader in the ESG and climate space to further penetrate into the fast growing market and further solidify its market position.

As such, in the current market environment that provides low returns, I think that investors should pivot to high-quality names like MSCI that is well positioned as an industry leader with a sticky revenue base and healthy business model, along with favourable tailwinds that will bring it through the storm. As such, my target price for MSCI is $567, implying a 36% upside from current levels.